find your solution.

search for solutions by category, industries, insights, and people.

find your solution.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

search for solutions by category, industries, insights, and people.

If there’s one thing our broad experience has taught us, it’s this: One size does not fit all.

Create a legacy for generations to come. Our seasoned advisors craft bespoke strategies for high-net-worth families and business owners, helping you preserve wealth, optimize tax planning, and secure a future that honors your achievements.

Our PE team provides valuable insight at every level of the investment cycle — from introduction to exit — for a wide range of middle-market customers.

Our healthcare team comprised of medical industry professionals seamlessly manages your business needs so you can devote your attention to patient care.

Guidance to propel you forward

From overarching strategy down to the details of your supply chain, we have over a century of experience and the skills to help you adapt to the market trends that drive manufacturing and distribution.

There are always ups and downs in the real estate market. We have a wealth of knowledge in investing, managing and developing property that provides valuable insights you need to navigate the ebbs and flows.

Lean on our nimble, proactive advisors who can adapt to shifting teams, timelines and trends, ensuring you’re covered from every angle.

Technology companies strive to stay ahead of the innovation curve by evolving and disrupting. Leverage our industry experience for actionable insights that lead to new opportunities.

Our professional services advisors bring a new point of view to your business while having a deep understanding of its nuances. Because, like you, we are in the business of building long-term relationships.

Combine our know-how with your drive to create meaningful impact for your community. Let us focus on your growth and finances while you fulfill your mission.

When conducting business globally, complex, multi-national challenges abound. We provide support and consultation for all of your international needs.

Keep up with the fast pace of the entertainment and sports industries with our team. We’ll take care of business so you can focus on your talent.

Our team provides customized solutions for your educational institution — no matter how large or complex.

Accounting Today

Accounting Today

Southeast’s fastest growing hubs as well as Bengaluru, India

The Centers for Medicare & Medicaid Services (CMS) Rural Health Transformation (RHT) Program represents the largest federal investment ever directed toward rural healthcare delivery. Authorized by the One Big Beautiful Bill Act, the program commits $50 billion over five years (FY 2026–2030) to help states stabilize and modernize rural health systems, expand access to care, and strengthen workforce capacity. To manage this multi-year effort, CMS established the Office of Rural Health Transformation, which monitors state transformation plans and supports the effective use of program funds.

The scale of the investment reflects the urgency of the challenge. According to an annual study by Chartis, more than 40% of rural hospitals are operating at a loss, with 417 facilities considered “vulnerable to closure.” Against this backdrop, the RHT Program presents a rare opportunity to address longstanding structural challenges. It also introduces new operational, financial, and enterprise-level risks and heightened accountability tied to the scale, duration, and oversight of the program.

Organizations that pair strategic investment with disciplined governance and internal control practices will be best positioned to convert grant dollars into lasting operational improvements and measurable community health outcomes.

The RHT Program distributes $10 billion annually to all 50 states through cooperative agreements administered by CMS. Half of the funding is allocated equally among approved states, while the remaining 50% is distributed based on factors such as rural population, the concentration of rural health facilities, and hospital-specific conditions within each state.

First-year awards range from approximately $147 million to $281 million per state, reflecting differences in rural health needs and the scope of proposed transformation initiatives.

Across states, funded initiatives commonly focus on:

Collectively, these investments are designed to transform rural healthcare delivery ecosystems rather than provide short-term financial relief.

For rural hospitals and healthcare providers, the RHT Program opens access to capital at a scale rarely available through traditional grant programs. States can tailor funding strategies to local needs, enabling providers to pursue shared services, regional partnerships, and coordinated care models that strengthen long-term viability.

Workforce development stands at the center of many state plans. Grant recipients can invest in recruitment and retention strategies, training programs, and expanded use of community health workers, pharmacists, and other licensed professionals.

Equally important, RHT funding supports modernization efforts, ranging from facility upgrades to advanced technology platforms, which allow rural providers to deliver higher quality care closer to home.

While the opportunity is significant, participation in the RHT Program materially changes the risk environment for rural healthcare organizations.

The RHT Program is administered as a federal cooperative agreement, requiring intensive oversight, annual reapplications, updated budgets, and ongoing reporting between states and CMS. Many states (e.g., New York) explicitly warn that this model demands substantial administrative effort from sub‑awardees.

For healthcare systems with limited administrative capacity, additional staffing for reporting, documentation, and compliance monitoring can increase overhead and divert resources from clinical operations with a CMS-mandated 10% cap on administrative activities.

RHT funding has strict limitations on how funds may be used. Funds may not be used to supplant existing clinical funding, support construction or major building projects, cover pre-award costs, or satisfy other federal matching requirements. As a result, providers must track costs carefully to avoid federal disallowances that could require repayment.

Projects that fall outside allowable categories may still be strategically important but must be funded by working capital or other means, increasing financial exposure and the potential for clawbacks if documentation fails to demonstrate full compliance.

RHT funding ends after FY2030, creating only a five‑year window for transformation. Services, technology platforms, and workforce initiatives launched with grant support must be financially sustainable once funding ends.

Without careful planning, hospitals may face post grant instability, particularly if new programs rely solely on RHT funding, lack ongoing revenue streams, or operate within already thin margins that limit the ability to absorb continued costs.

Many rural providers enter the program with pre-existing financial strain, including high costs, limited market power, small economies of scale, constrained liquidity, and structural balance sheet weaknesses.

Grant participation requires upfront investment or co-investment, while reimbursement timing can create cash flow pressure. For organizations already operating with thin margins, these dynamics can unintentionally compound financial stress rather than alleviate it.

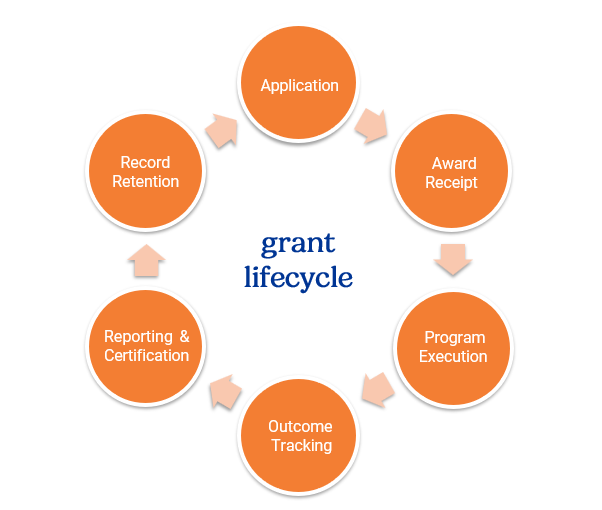

Taken together, these risks can reflect a fundamental shift in operating reality for rural healthcare organizations, as the scale, duration, and oversight of RHT funding elevate risk and require intentional governance and disciplined internal controls throughout the grant lifecycle.

Large federal grants bring expanded compliance, financial, and operational obligations. As stewards of public funds, recipients must maintain structured oversight and accountability aligned with CMS expectations. For rural hospitals and healthcare providers receiving RHT-related funding, this requires disciplined financial management and monthly, state-level compliance reporting on individual grants, covering expenditures, progress against approved plans, and required certifications.

Strong internal controls are not only a federal requirement, but a foundational risk management necessity, safeguarding public funds and helping to protect providers from operational, financial, and reputational harm. A well-designed grant internal control framework provides end-to-end oversight across the grant lifecycle, promoting transparency, strengthening risk management, and supporting program performance from application through closeout as compliance demands intensify.

An effective framework focuses on:

Risk begins at application and continues through closeout. Effective internal controls provide continuous oversight across the grant lifecycle, creating a structured environment where operational, financial, and compliance risks are identified, monitored, and mitigated.

Hospitals and healthcare providers that extract lasting value from RHT funding will approach it as a multi-year transformation initiative, not a one-time infusion of capital. Practical strategies include:

Strong controls help providers connect grant spending to long term operational resilience and community health outcomes.

The Elliott Davis Healthcare team supports rural hospitals and healthcare providers across the full grant lifecycle, from strategic planning and application support through compliance, governance, internal controls, and post-grant closeout validation. Our integrated approach helps organizations strengthen accountability while maximizing the long-term value of transformative federal funding.

Contact us today to start the conversation and learn more about the tools and processes we’ve built to support this initiative.

The Centers for Medicare & Medicaid Services (CMS) Rural Health Transformation (RHT) Program is one of the most significant federal–state healthcare funding initiatives in decades. Authorized under the One Big Beautiful Bill Act, the program commits $50 billion over five years (FY2026–FY2030) to support new approaches to improving access, sustainability, and outcomes in rural healthcare.

Once a state releases its Notice of Funding Opportunity (NOFO), organizations often have a short window, sometimes as little as six weeks, to assemble partnerships, design projects, and submit applications.

The organizations best positioned to benefit are those that treat RHT not as a grant-chasing exercise, but as a five-year transformation effort that requires planning well before funding announcements are released.

The RHT Program is federally authorized and implemented by states, making it distinct from traditional Medicare or Medicaid funding models and signaling a possible evolution in how public healthcare gaps are addressed.

This structure allows RHT to pick up where Medicare and Medicaid leave off, enabling states to direct funding toward access challenges that existing programs do not fully address. Rural communities often face fewer providers, longer travel distances, and limited care options. With roughly 20% of the U.S. population living in rural areas, RHT focuses on workforce investment, technology adoption, care delivery redesign, and regional collaboration to close persistent access gaps.

RHT funding also reflects broader federal fiscal dynamics. Reductions in federal healthcare spending have increased pressure on states to deploy RHT dollars thoughtfully and defensibly. As a result, the program is not only a near-term funding vehicle, but a policy experiment that may inform how future federal–state healthcare initiatives supplement core entitlement programs.

Although RHT is federally authorized, it is designed and implemented at the state level. Each state develops its own priorities, funding structures, and application processes.

For rural hospitals and healthcare providers, this means strategy must account for:

Successful applicants position their proposals as part of the broader transformation agenda the state is advancing.

It’s also important to recognize that funding is not required to flow directly to rural providers, and there is no single national playbook governing how funds are awarded. As a result, success depends on understanding state intent and translating those priorities into well-aligned, defensible proposals.

States that have already released RHT guidance or early NOFOs provide important clues about how funding decisions are likely to be made.

Across early adopters, several themes are emerging:

Organizations that wait for the NOFO often underestimate the internal control, compliance, and reporting infrastructure required to responsibly manage RHT funding.

Many state RHT requests for proposals are expected to open April–June, often with 45–60 day submission windows. Once a NOFO is released, organizations may have only weeks to:

That timeline limits strategic decision-making. Some choices simply cannot be made well in six weeks, particularly those involving multi-year operating models and workforce capacity.

RHT funding is time-limited. Strategic planning should extend beyond award and implementation to how programs will be funded after grant dollars expire. Organizations should evaluate whether new services generate ongoing revenue or measurable cost savings, and how workforce and technology investments fit within long term operating models.

Treating RHT as a multi-year transformation arc, rather than a one-time funding opportunity, helps reduce the risk of post grant instability.

Before applying, organizations should have clarity on:

Internal alignment accelerates decision-making once state guidance is released. Without it, even strong opportunities stall. Failure to align projects with how states ultimately measure success may also expose providers to funding reductions or clawbacks.

RHT funding can materially change the financial profile of an initiative and how it should be prioritized. Ultimately, strategic decisions come down to how an organization allocates its time and money. When those resources are misallocated, the consequences can be significant.

For example, consider a project that initially ranked low as an organizational priority because it delivered a 10% internal rate of return (IRR). If that same project receives RHT funding over five years, even after accounting for added compliance costs, its projected IRR could increase to 25%, elevating it to a top-tier priority. See the illustrative example below.

This reframes prioritization decisions as lower-priority initiatives may become financially compelling, and “shovel-ready” projects can take on new urgency. For the leadership team, RHT should alter how initiatives are evaluated, not simply which grants are pursued.

RHT compliance requirements are often underestimated. Each grant carries its own reporting cadence, performance metrics, and repayment provisions for noncompliance. If required data is incomplete or reported outcomes fail to meet defined thresholds, grant funds may be subject to repayment, even if services have been delivered.

In many cases, organizations face structural gaps that heighten the risk:

For multi-state healthcare systems participating in hundreds of state-specific grant programs, these challenges compound quickly, increasing exposure and straining already limited administrative capacity. Underestimating the compliance costs will overstate expected ROI and could result in poor allocations of capital that put the organization at risk and strain finances.

Early engagement can influence outcomes when approached with intention. A proactive strategy may include participation in regional collaboratives, state-level outreach to understand priorities, and early conversations with potential partners.

Elliott Davis works with rural healthcare providers across the full RHT lifecycle, including:

We help organizations decide which opportunities to pursue, prepare to respond quickly, and support the operational discipline required to retain funding and deliver lasting value.

Contact us to start the conversation.

For many closely held businesses, particularly in construction and manufacturing and distribution, employee stock ownership plans (ESOPs) have become a compelling succession planning strategy. When a third-party sale is not the right fit, an ESOP can provide liquidity to owners, preserve company culture, and give employees a meaningful stake in the company’s future.

Once the transaction closes, there are important financial aspects that companies should proactively consider. The first year-end after an ESOP transaction introduces a different rhythm to accounting, audit, and tax planning. Companies that step back, understand the big picture, and coordinate early tend to move through this period with fewer challenges.

An ESOP transaction changes how the company thinks about ownership, cash flow, and financial reporting. While manageable, these considerations do require adjustment. Companies that navigate this phase effectively approach the first year-end as an extension of the transaction, with key accounting, valuation, and tax elements continuing into the reporting cycle.

Post-transaction change often shows up in three areas:

Understanding these differences from the beginning sets the right tone for the years ahead.

The first year after an ESOP sale focuses on setting a baseline, as opening balances, new equity accounts, and revised debt structures come together to support future reporting. In leveraged ESOPs, companies also manage both internal ESOP loans and external financing, often involving sellers and/or banks, which affects how transactions are recorded and presented in the financial statements.

In some cases, the structure includes a holding company, adding intercompany activity and consolidated reporting to daily accounting responsibilities.

Companies should also plan for technical accounting requirements under Generally Accepted Accounting Principles (GAAP) associated with ESOP transactions. Common areas that require attention include:

An ESOP naturally expands audit considerations. Auditors now need to understand how shares are valued and allocated, how debt is serviced, and how employees become eligible participants over time. In the first year, audit planning carries as much weight as execution. Timing of the transaction, expectations of lenders or bonding companies, and reporting deadlines all influence which periods are audited and how work is sequenced.

Late alignment can strain internal resources. Early coordination among audit, accounting, and valuation teams creates a more predictable and manageable process. Companies should also be mindful that certain services may raise independence considerations, making early coordination across providers even more important.

ESOP ownership can create meaningful tax advantages, especially when companies take a longer-term view beyond the first year.

At the shareholder level, some sellers may qualify for capital gains deferral, adding another layer of coordination between personal planning and company planning. That alignment often carries into broader tax planning, with many ESOP-owned companies using the first year to establish an approach that supports growth, reinvestment, and long-term employee ownership.

The first year of ESOP ownership often reveals challenges that stem from timing and coordination. Common pressure points include:

The most effective countermeasure is setting clear valuation timelines, agreeing on audit expectations, and coordinating among advisors well early on in the process. In doing so, leaders who understand how ESOP ownership affects cash flow, reporting, and debt service are better equipped to make coordinated operational and financial decisions.

Elliott Davis supports ESOP-owned companies through every stage of the business lifecycle. Our team works closely with management, trustees, and valuation firms to align accounting, audit, and tax considerations with broader business goals.

If you are approaching your first-year end after an ESOP transaction, proactive planning can reduce risk, improve reporting outcomes, and ease the transition into ESOP ownership. Contact us today to get started.